Build Your Emergency Fund💰

Why you need it, how to store it and when to use it - a detailed guide on emergency funds

Hello, and welcome to Reflections. I'm Sanuj, a physician. I write insightful posts about health, wealth, family and other interesting topics. If you're new here, you can learn more about Reflections in the about page. If you would like to read more, hit the subscribe button below to catch my weekly posts and join a growing list of readers around the globe.

It goes without saying that life is a risky journey. Whatever we venture into, despite good intentions, can backfire. The same applies to our finances. We invest in various asset classes, some calculative and some speculative. Risk is an inherent part of investment, although the degree of risk may vary. When faced with such a risk, what we can call as a ‘financial crunch', how do we take care of our necessities? If you are part of a family, you may need money for rent, school fees, food, electricity, and so on. Or your work involves a gadget like a smartphone or a laptop and it decides to call it quits one day. These gadgets are expensive and replacing it is a sudden unforeseen expenditure. Maybe you're a bachelor or bachelorette and don't have the burden of familial expenses, but you still have needs for yourselves. Say you have a loan to pay and you lose your job. You don't want the bank to seize your assets. All of these situations sound like a financial emergency. This is where your emergency fund comes in to save you, but only if you have one.

An emergency fund is your backup money that is created when you understand that you can expect the unexpected at any time. It is the financial lifeline in times of an economic downturn in our personal lives. An emergency fund protects against unforeseen expenses, reduces financial stress, prevents high-interest debt, and maintains financial independence. Additionally, it supports long-term financial goals, and enhances employment flexibility.

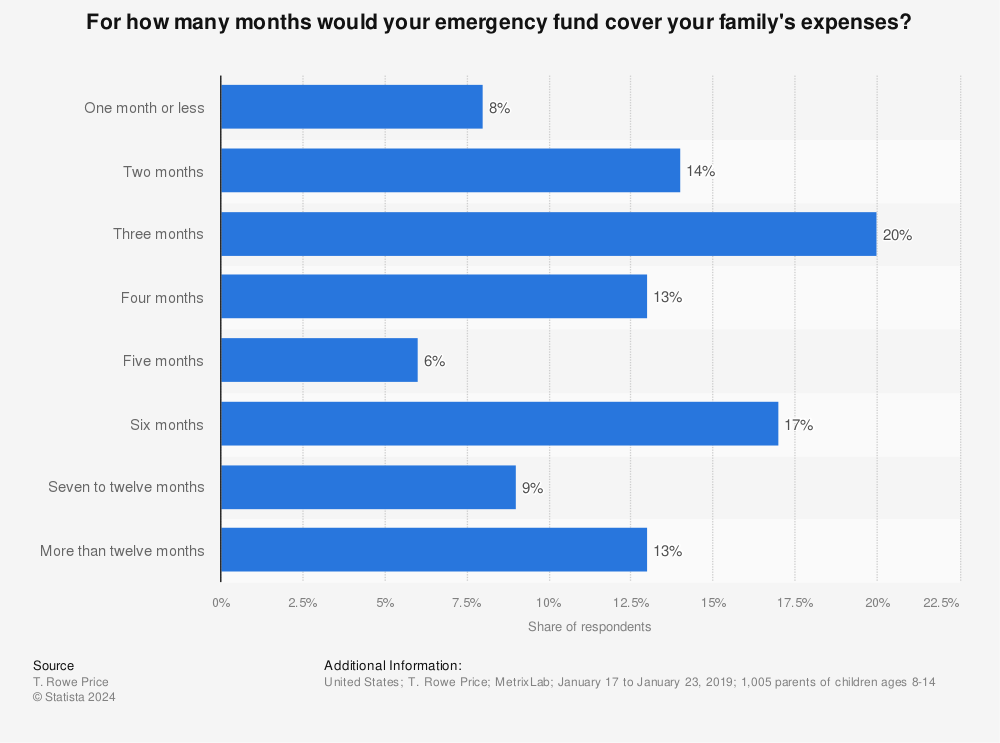

Unfortunately, the percentage of people prepared for such emergencies are miniscule. Data from the USA suggests that only 17% of people had at least 6 months of emergency funds and only 9% of people had at least 7-12 months of emergency funds to cover for their family’s expenses.

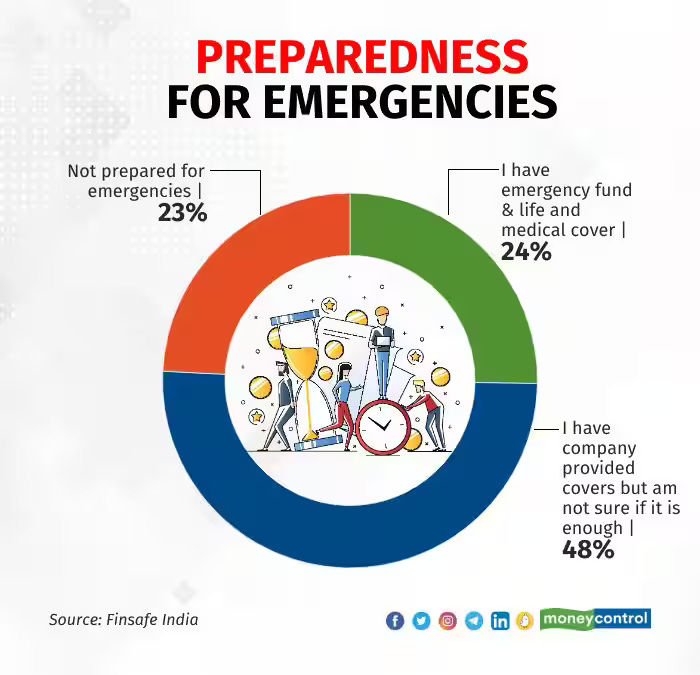

In India, only a meagre 24% were financially prepared to face an emergency.

All of us need an emergency fund. There are no two thoughts about it. The big question is how do you build your emergency fund and where do you keep this money?

How do I Build an Emergency Fund?

The financial needs of every person is unique. Therefore, the amount needed to keep aside for emergencies would differ from person to person. In building an emergency fund, you would have to calculate all the unavoidable expenses that you would require for a month. Avoidable expenses like dining in an expensive restaurant, vacations and movies need not be included, because they're, obviously, unnecessary during a financial crisis. Stick to the money you would require for a month to fulfill your needs and not wants. Let's call this amount X. Atleast 6 and preferably 12 times X is what you should keep as an emergency fund. That is you should have enough money to sustain all your needs including your family’s needs, if they are dependent on you, for 6-12 months.

You are unlikely to build in one month an emergency fund that lasts for 12 months. Therefore, the best thing to do is to keep building it as you earn till you reach your desired calculated amount (6X to 12X, mentioned earlier). For example, if your calculated emergency fund requirement is 1 lakh rupees, try to set aside ₹10,000 per month till you reach your target. A higher portion may have to be kept aside monthly for those with a higher emergency fund requirement.

Where do I Keep This Emergency Fund?

First and foremost, an emergency fund is not created to grow your wealth so don't expect your money to double or triple. It is made to act as cushion against a stressful financial situation. In this regard, an emergency fund should always be maintained in safe or relatively safe assets from where you can withdraw the amount easily. But do remember that you also don't need to use an emergency fund frequently. This means you could keep a portion of the fund in safe asset classes that offer slightly higher interest rates than a simple savings bank account.

Here are some of the asset classes that could be considered to store (for quick and easy retrieval) your emergency fund.

1. Savings account

Your savings account is the best place to store a portion of your emergency fund for instant access. You could use UPI/Google Pay (linked to your savings account), your debit card or simply withdraw cash from an ATM.

2. Liquid Mutual Fund

A liquid mutual (debt) fund is called so because your money is, well, liquid here. You can withdraw at any time. They invest in bonds or debt instruments, including government treasury bills in India, that mature in 91 days. The credit quality of the debt instruments in a liquid fund are usually excellent. This makes both credit risk and interest rate risk minimal, leading to low volatility, providing a relatively safe asset class. The interest here is slightly higher than that received from a savings account and may occasionally be at par with the interest on fixed deposits. There are no additional charges for withdrawal. These funds have a minimal expense ratio and you are taxed for these funds only at the time of withdrawal, unlike a savings account or fixed term deposit account where the interest is taxed annually.

3. Fixed Term Deposit

Although not as liquid as a savings fund or a liquid mutual fund, fixed term deposits are still an option to save a fraction of a your emergency fund corpus. They occasionally give inflation beating returns (which may get cut down further post tax). They can be redeemed on any business day even before maturity although you may have to pay a penalty for early withdrawal. The money is usually tied to banks and in India, term deposits upto 5 lakhs rupees in a bank are insured by Deposit Insurance and Credit Guarantee Corporation as dictated by the Reserve Bank of India.

4. Arbitrage Mutual Funds

Arbitrage mutual funds are a type of mutual fund that aim to generate returns through arbitrage opportunities in the equity markets. Arbitrage involves simultaneously buying and selling the same asset in different markets to take advantage of price differences. Imagine there's a stock of a company, ABC. In the cash market (where you buy and sell stocks immediately), the price of ABC stock is ₹100. In the futures market (where you agree to buy or sell stocks at a future date), the price of ABC stock is ₹105. The arbitrage mutual fund manager can buy in the cash market and sell in the futures market to gain a profit.

This strategy, which involves buying and selling simultaneously, minimizes the risk of losing money due to market fluctuations. Arbitrage funds fall under equity mutual funds and hence, you are taxed only at the time of redemption. A portion of your emergency fund could be allocated to arbitrage mutual funds to potentially earn higher returns than a regular savings account, while still maintaining a low risk profile. Redemption of money takes longer than a regular savings account, liquid fund and fixed deposit. Therefore, don't invest your entire emergency fund corpus here even if it is to save taxes.

Remember to Replenish your Emergency Fund

We may land up with a financial emergency at some point in our lives and either exhaust or partially exhaust our emergency fund. During the COVID - 19 pandemic, nearly 14% of Americans wiped out their emergency savings. If you face such a situation, you may eventually get back to receiving a steady income. When that happens remember to replenish your emergency fund at the earliest to prepare yourself for the next financial emergency.

One extremely important piece of advice would be to never use your credit card when you have a financial emergency. It is only going to add to your financial burden due to the exorbitantly high interest rate on default. So start building an emergency fund, diversify it among various ‘safe’ asset classes and sail through a financial crunch without any major setbacks.

A Quick Update

I have turned on paid subscription on Substack. However, all new posts will continue to be free. It is a nominal amount to show your support to a writer.

If you don't want a full subscription but would still like to support me, you can buy me a coffee for just $2 by clicking on the link below. Your support motivates me to continue creating insightful posts. A portion of the proceeds will go towards charity.

⚠️Disclaimer: This newsletter is purely for informational purposes only and does not constitute financial advice, investment recommendations, or an offer to buy or sell securities. Investing in equity markets carries inherent risks, and past performance is not indicative of future results. Readers are encouraged to consult with a qualified financial advisor and conduct their own research before making any investment decisions. The author and publisher of this newsletter are not responsible for any financial losses or decisions made based on the information provided herein.